# BackTest on Bitcoin using three Relative Strength Index (RSI) lengths with Python

• The data set was used from yahoo!-finance. (2020-01-01 ~ 2025-06-14)

• Do backtest on bitcoin to compare between RSI length 14, 20, and 30 in 4 hours, daily, and weekly cycles.

• Standard : Buy when RSI < 30, Sell RSI > 70.

• Compares to Buy & Hold

• Demonstrate cumulative return, Sharpe ratio, and MDD.

# Summary for RSI Strategy Backtest vs Buy & Hold (BTC, 2020 ~ 2025)

After running backtests on RSI-based trading strategies using lengths 14, 20, and 30 windows across different timeframes, several key insights emerged when compared to a simple Buy & Hold approach on Bitcoin from 2020 to 2025.

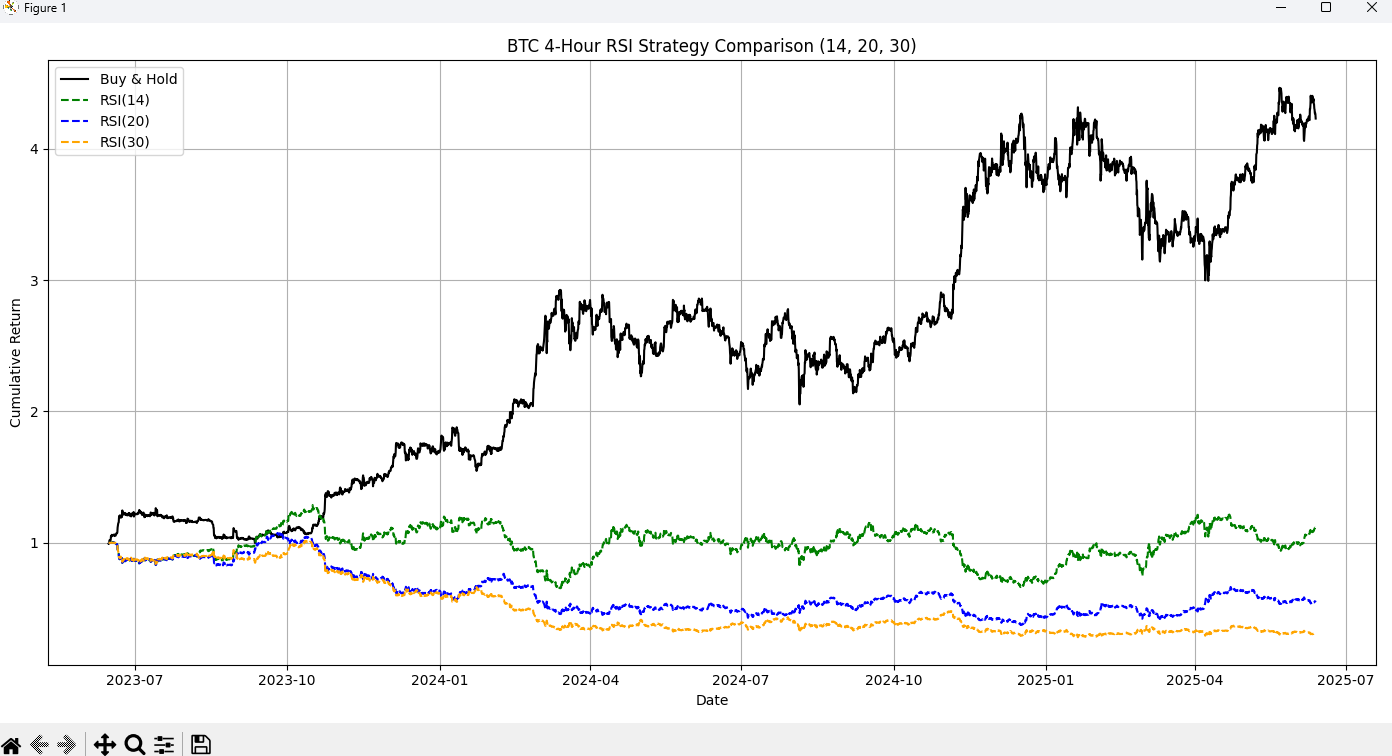

▸Bitcoin RSI Strategy Comparison (14, 20, 30) in 4-hour timeframe

◦ On 4-hour timeframe, RSI(14) showed more moderate success than RSI(20) and RSI(30).

◦ However, Buy & Hold still yielded better overall returns in most cycles.

◦ RSI(30) on the 4 hour chart was consistently underperformed.

◦ However, Buy & Hold still yielded better overall returns in most cycles.

◦ RSI(30) on the 4 hour chart was consistently underperformed.

Conclusion

Among all RSI strategies, RSI(14) on the 4-hour timeframe demonstrated the most potential for active traders. However, without the additional optimization, it still trails behind Buy & Hold over the long-term.

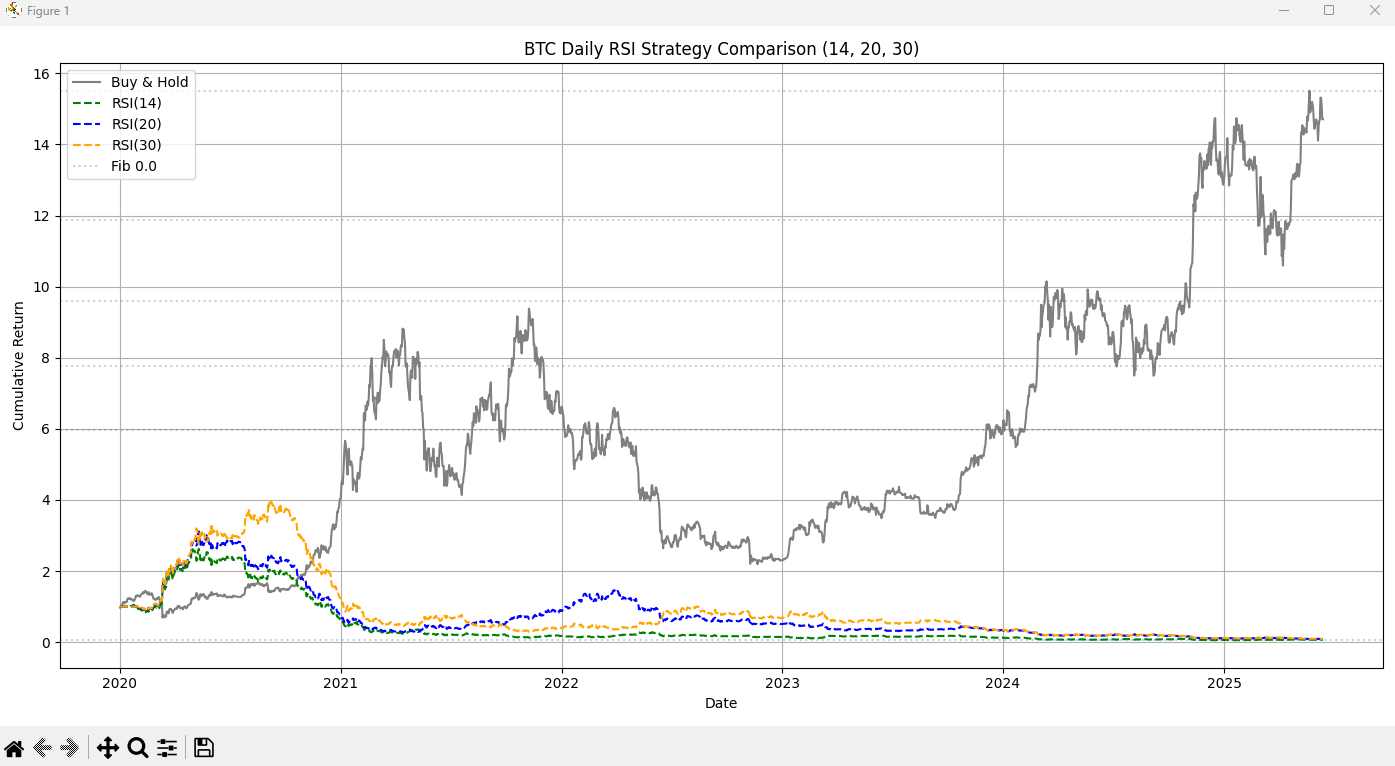

▸Bitcoin RSI Strategy Comparison (14, 20, 30) in daily timeframe

◦ RSI(30) initially performed great during early trends but it failed to maintain gains. (2021 ~ 2022)

◦ The Buy & Hold strategy significantly outperformed all RSI-based strategies over the long-term. This gave over a 15x cumulative return.

◦ All RSI strategies struggled during bear markets and often missed major bullish trends.

Conclusion

RSI on daily timeframes showed some downside protection but it underperformed during strong uptrends. It was reactive rather than predictive.

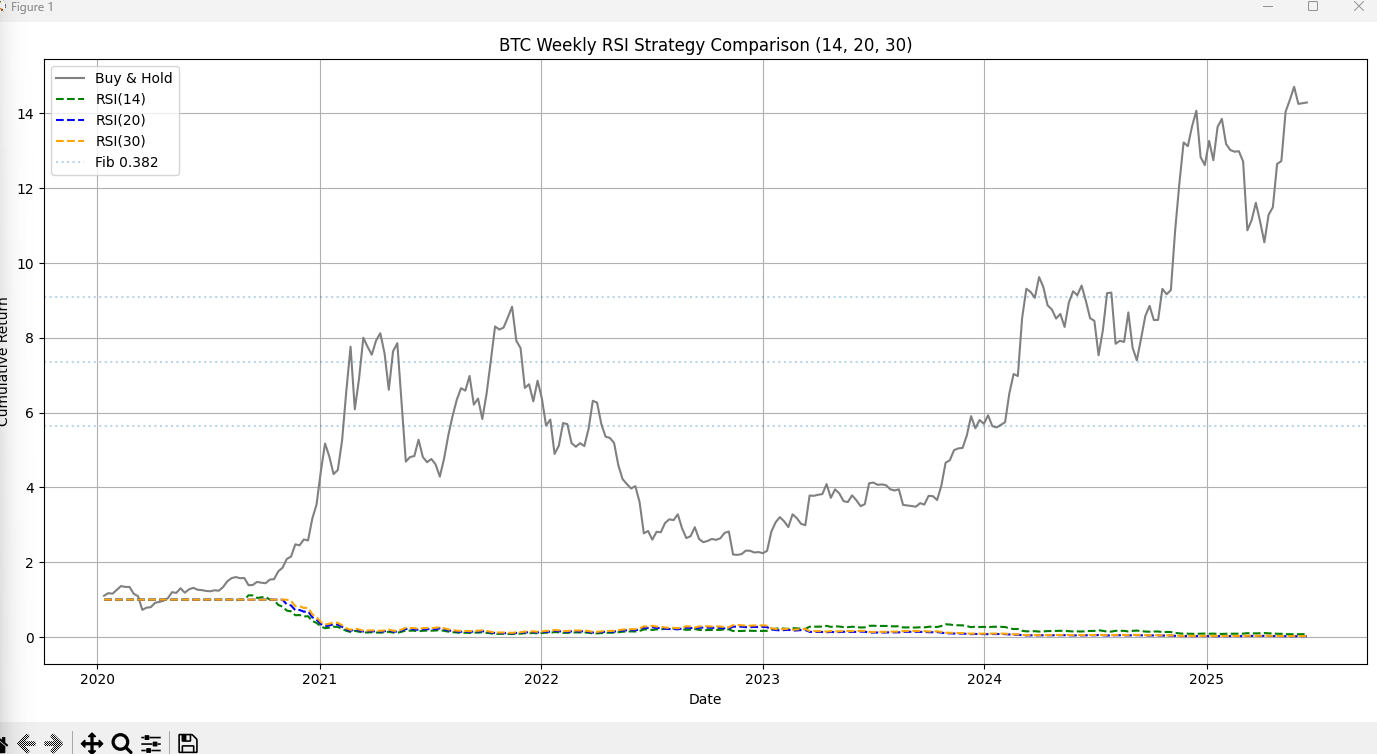

▸Bitcoin RSI Strategy comparison (14, 20, 30) in Weekly cycle

◦ Buy & Hold continued to show strong long-term returns.

◦ Weekly RSI signals were too infrequent and too late to capitalize on major price moves.

◦ Most trades triggered on weekly RSI were either flat or unprofitable.

Conclusion

The weekly cycle was too slow for timely entries and exits. RSI did not provide meaningful edge over passive holding.

▸Overall, among all RSI strategies, RSI(14) on the 4-hour timeframe demonstrated the most potential for active traders.

However, without the additional optimization, it did not fully capture the market's upside in the long-run.

On the other hand, Buy & Hold remains the most profitable strategy in Bitcoin from 2020 to 2025 without high volatile.

However, without the additional optimization, it did not fully capture the market's upside in the long-run.

On the other hand, Buy & Hold remains the most profitable strategy in Bitcoin from 2020 to 2025 without high volatile.

I would do RSI with other indicators (e.g., moving average and volume) for solving this problem after July 2025.